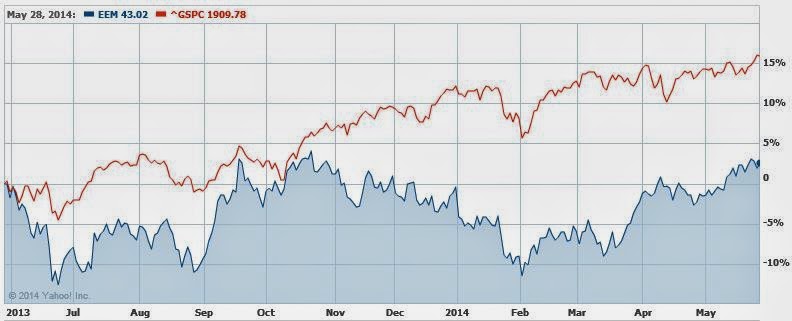

Emerging economy stocks as a group are booming. In the week of May 21, emerging market stocks attracted another $1 billion of inflows even as U.S. equity funds saw withdrawals of $10.9 billion. This data comes from EPFR, a company that tracks the flow of money into and out of world stock markets. The firm adds that this weekly addition marks the seventh week of net inflows in the past two months. From February 3 through May 23, the iShares MSCI ETF for emerging markets (EEM) has soared 16.2% whereas the Standard & Poor’s 500 Index has risen 9.1%. Leading the emerging markets higher has been India, where the expectation of favorable national elections propelled its market to a gain of 32.2% during this period. The popular ETF for Brazil (EWZ) rocketed 25.8%. The question for investors is whether these emerging markets will continue to advance and to also outpace U.S. stocks.

This surge in emerging markets has surprised many investors due to the widespread assumption that the Federal Reserve’s “tapering” policy, now in its sixth month, would damage emerging markets. This view goes back to the announcement on May 22, 2013 by then Chairman Bernanke that an expected pickup in the U.S. economy would permit the Fed to wind down its policy of purchasing $85 billion of bonds per month, which had been designed to put downward pressure on long-term rates and support the mortgage market.

Bernanke’s statement had an immediate and dramatic impact: U.S. bond yields rose and the dollar strengthened against many emerging currencies. This in turn led to fears that currency, inflation, and interest rates would rise, economic growth would slow, capital outflows would increase, and equity markets would decline in some key emerging countries. In the month following Bernanke’s remarks the EEM plunged 14% whereas the S&P 5900 Index declined only 4.7%. Conditions continued to deteriorate during the summer, which in late August prompted Christine Lagarde, Managing Director of the International Monetary Fund (IMF), to warn the Fed to be highly sensitive when initiating its tapering policy to a possible adverse reaction within emerging countries.

At this point, the EEM has managed to recoup all of the losses incurred since Bernanke’s speech a year ago, yet the EEM’s gain of 1.2% trails the 15.1% advance of the S&P 500 Index over the last twelve months. It seems obvious that the Fed’s tapering policy, on its own, is no longer sufficient to cripple emerging markets. On the other hand, it appears that it is when tapering combines with other developments to drive the yield on the benchmark 10-year U.S. Treasury notes and the dollar up, as was the case in mid-2013, that there is a negative causal impact on emerging markets. Since February 3, the opposite has happened. The yield on the 10-year Treasuries has fallen slightly from 2.58% to 2.53%. Also, the net asset value of the PIMCO Emerging Markets Currency Fund (PLMIX) has risen from 9.87 to 10.37, a gain of 5.1%.

The Marietta economic outlook includes a probable rise in the 10-year Treasury yield as the U.S. economy continues to strengthen in the second half of the year. If this occurs, and is accompanied by a rise in the dollar vs. emerging currencies, there will likely be a sterner test for emerging stock markets. This would especially apply to those countries with a recent history of inflation and currency woes (India, Brazil, Indonesia, South Africa, Turkey, et al.). On the other hand, from a fundamental perspective, a stronger U.S. economy and rising U.S. stock market may well be viewed as a positive for emerging markets in that it will increase investor confidence in the global economic growth scenario and boost their willingness to invest in the perceived higher risk associated with emerging markets. This is what happened in the booming markets from 2003 through 2007.

Our conclusion is that it is appropriate for investors to increase modestly their exposure to emerging country stocks in the currently more favorable conditions. If the U.S. economy strengthens and longer term interest rates rise, as we expect, and key emerging market stocks continue to rise, then a larger commitment is justified. An important caveat: not all emerging economies will react similarly to propitious conditions. China, for example, has a unique set of conditions such that Federal Reserve policy changes and interest rate fluctuations will likely have a reduced impact on its more insulated economy and markets. We recommend countries which are expected to experience an improved mix of accelerating GDP, stable or rising currencies, stable and preferably declining inflation and interest rates, and a growth-oriented government and central bank.